Taiwan’s Textile and Garment Industry under Globalisation

Youth Labor Union 95, Taiwan

Written by: Chia-Wei Liang

Reviewed by: Ray Cheng

Editor: May Tam

Foreword

The textile and garment industry is one of Taiwan’s important manufacturing industries. It is also a crucial source of supply for the world’s garments and textile products. This research report reviews the history of the industry’s development in Taiwan since the end of World War II (WWII), looks at its present situation and the role it plays in the global production chain. The report also examines how the Covid-19 pandemic emerged in 2020 has affected the industry and how the sector responds to the challenges.

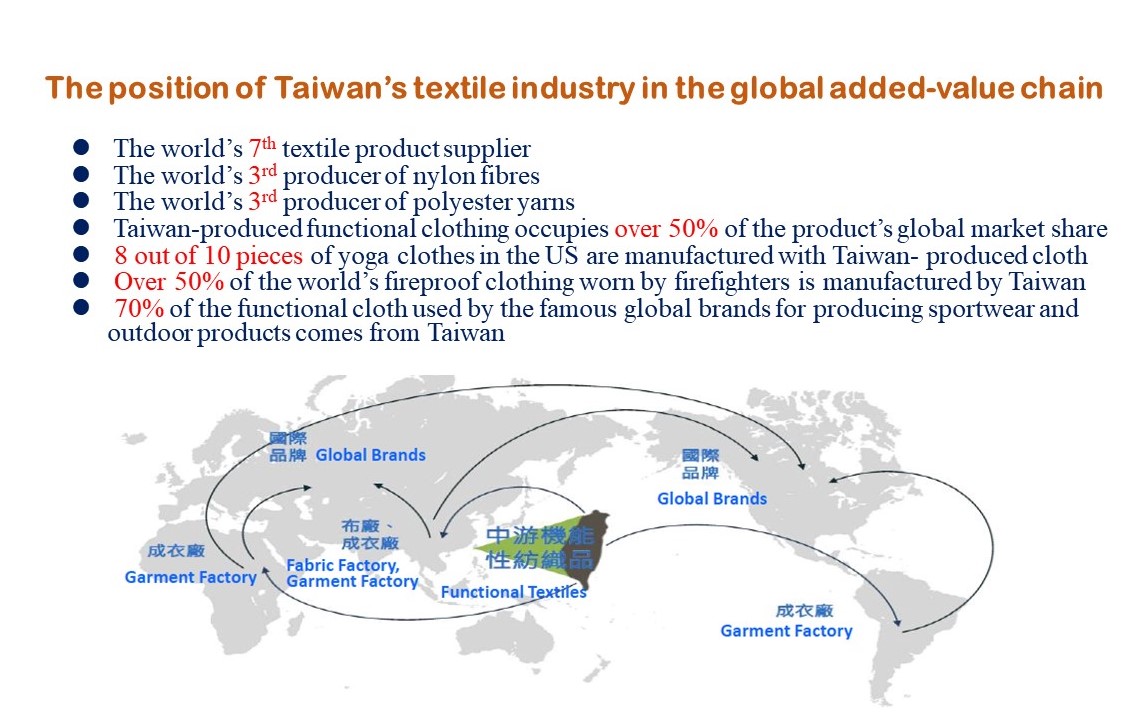

I. The present situation at a glance

Before reviewing the development history of Taiwan’s textile and garment industry, let’s take a glance on its role and status in the world today. The Taiwan official statistics of 2019 have told about the industry’s global importance which is expressed in the following two graphics.

The above statistics show that Taiwan’s textile is the crucial supply source of production materials for global garment brands, particularly on sportswear and functional clothing like fireproof wear. Taiwan’s textile and garment enterprises set up factories abroad including Mainland China, Southeast Asia and South America to manufacture textile products and OEM garments. The industry mainly focuses on textile whereas garments share only a relatively tiny part of the business. More details about the industry’s present situation are described in section III below.

II. A brief development history of the industry

It can be summarised in six phases:

1. The early phase(1945-1960)

The output value and the number of factories for Taiwan’s textile industry after WWII were scarce and the supply of such products depended on imports. Yet, changes in the world’s economic and political order in the 1950s had brought opportunities for the industry to kick off development in Taiwan. On the economic side, the manufacturing cost of garments in Europe, the US and Japan had been rising whereas Taiwan’s wages were relative low, and thus the production was shifted to Taiwan to help reduce cost, which had created enormous job opportunities in Taiwan. Taiwan Government hence rendered significant support to the industry. For the world politics, the Korean War broke out during the period. The US contained China and the Soviet Union, but assisted Taiwan through exporting to it massive amount of materials including cotton, which prompted development and export of Taiwan’s cotton textile products. In 1959, Taiwan’s export of textile products amounted to more than USD13 million, equivalent to 12% of Taiwan’s total export value.

2. The phase of export extension to other products(1961-1967)

In 1960s, the US and Canada imposed quota on the entry of Taiwan’s textile products in 1961 and 1963 respectively after their markets had been badly hit by the previous massive Taiwan import of the products. As a result, Taiwan shifted production of cotton textile products to artificial fibres which were made from petrochemical materials. Moreover, the US also stopped its assistance to Taiwan in 1965 and thus its supply of cotton to Taiwan dropped. The Taiwan Government subsequently adjusted the development direction and policy for its textile industry, with a shift of production to artificial fibres.

3. The phase of export expansion(1968-1974)

This was the glorious period when the garment production had been developed from its previous labour-intensive nature to a full-grown system comprising upper-, middle- and lower-stream operations. Although facing the pressure of rising wages and the entry of low-price commodities to the world market from the developing countries employing low-paid workers, Taiwan was not heavily struck as its textile and garment industry had become self-sufficient by then with its cost reduced by mass production.

Taiwan replaced Japan to be the premier base of Asia’s textile industry which had become Taiwan’s most important industry for export earning foreign exchange, with the export value of textile and garment products amounting to over 30% of Taiwan’s total exports. Taiwan at that time, together with Hong Kong, Italy and South Korea, were ranked as the world’s top four exporters of textile products.

4. The phase in response to quota challenge(1975-1986)

The development was slowing down mainly due to the oil crisis as well as quota imposed by a number of countries on Taiwan’s export of garments, textile raw materials and manufactured goods.

5. The phase of maturity and downturn(1987-2001)

Factors leading to the downturn were varied, such as surging prices of raw materials for textile production, increasing workers’ wages, labour shortage, arising environmental awareness, appreciation of Taiwan dollar (NTD) and low cost in the emerging textile manufacturing countries.

In 1987, the Taiwan Government permitted overseas investment, and the manufacturing sector started moving factories overseas to reduce cost. The globalised model of “Receiving orders in Taiwan, Manufacturing overseas, Exports to a third place” had gradually been established. The places for investment in the early stage were Southeast Asian countries such as Malaysia, the Philippines and Thailand. Some factory owners moved production to countries like Mexico, Nicaragua, South Africa and Sri Lanka in response to restrictions from the US quota. In 1989, the Taiwan Government allowed investments on Mainland China, which had commenced the tide of setting up manufacturing plants in China.

Moving the industry operation outward had caused the sector’s production value growth rate to drop from 11.3% in 1991 to less than 1% in 2000.

6. The phase of technology transformation(2002-)

Since Taiwan’s entry to the World Trade Organization (WTO) in 2002, its textile export value has been dropping year after year. The reasons include global competition encountered, challenges from the low cost of those countries emerging after the cancellation of the textile quota system, as well as the heavy blow brought by the global financial tsunami in 2008. However, Taiwan’s such an industry still occupies a significant position in the world. Taiwan was the world’s top 6th exporter of textile products and the 29th exporter of garments.

The Taiwan Government has been actively supporting the industry by initiating at least four schemes to boast its competitiveness, enhance integration of its upstream and downstream operations, and facilitate its brand building.

III. The present situation

1. Output value

-

During the 10 years between 2009 and 2018, the output value of the upstream business of raw materials was much larger than that of the downstream garment production. The output value of artificial fibres over the period was mostly more than NTD100 billion per year, while about NTD300 billion for textile and less than NTD30 billion for garments which was pretty low.

2. Imports and exports

- In 2019, the sector’s export value was USD9.18 billion and import value USD3.53 billion, ending up with a trade surplus of USD5.63 billion. The industry is Taiwan’s top 4th one bringing trade surplus.

- The largest export product category is fabric, followed by yarns and fibres. This shows that the up- and mid-stream of production material manufacturing forms the main business of the sector. In 2018, Taiwan was the world’s top 7th exporter of textile products, with an export value of USD9.2 billion, and its supply of functional and environmental protection related textile products standing at a prime position in the world (See Section I). The largest importers of this Taiwan industry’s products were in order the ASEAN (Association of Southeast Asian Nations) member states, China-cum-Hong Kong and North America.

- In 2019, the sector’s imports were mainly garments, with a value of USD1.946 which equalled to 55% of the sector’s total import. The second and third largest imported textile items were fabric and fibres respectively.

3. Enjoying an important global status yet with a wait-and-see outlook

- Taiwan’s artificial fibres and functional fabric occupy an important position in the global supply chain. However, the values of production and sales had continuously gone downward during the years of 2015-2017, but rose a bit in 2018 and fell again in the first half of 2019. Thus the outlook is still wait-and-see.

IV. The industry under the pandemic

-

Taiwan’s textile and garment industry had been seriously hit by the Covid-19 pandemic in 2020. For example, the Tokyo 2020 Olympic Games could have called for massive production of sportswear and functional fabric from Taiwan, but the call-off of the event in the year due to the pandemic had caused Taiwan’s textile factories to suffer tremendously.

-

The textile trade slipped apparently. The sector’s export value in the first nine months of 2020 was USD5.443 billion, a decrease of 22% compared with that in the corresponding period of the previous year, while the import value was USD2.453 billion with a drop of 7%.

- The worst period was between April and July 2020, but a rebound appeared after August upon the alleviation of the pandemic.

- In response to the challenges brought by the pandemic, several large enterprises, such as Far Eastern New Century, Eclat Textile, Makalot, Singtex, New Wide Group and Everest Textile, have quickly shifted production to anti-epidemic items such as protective clothing and face masks. Some of them add fashionable elements to the fabric they are producing while some have developed new anti-pandemic products. For instance, the Far Eastern New Century has changed production to the manufacture of medical barrier gowns, and plastic sheets which are used for making protective face masks. Such a move has brought good profits. Now the enterprise has become the world’s biggest supplier of medical-used composite fibres of PE/PP and PE/PET. It also prepares to grasp the new business opportunities of medical and hygiene material production, which has become a development direction of the company in the post-pandemic era.

V. A brief summary

The textile and garment industry is one of the important manufacturing industries in Taiwan. It also occupies a significant position in the world and is a crucial supply source of production materials for international garment brands, particularly on sportswear and functional clothing such as fireproof wear.

The industry began to develop after WWII. In 1950s, the high production cost of garment manufacturing in Europe, the US and Japan prompted a shift of the production from these places to Taiwan. At the same time, the US confronting China and the Soviet Union whereas assisting Taiwan led to a large export of the US cotton to Taiwan, which prompted development and export of the island’s cotton-made products during the period. However in the 1960s when the US assistance to Taiwan came to a halt and quota systems adopted overseas had compelled Taiwan to shift production from cotton-made products to artificial fibres. The industry later entered a glorious period in the 1970s when a full-grown system comprising the up-, mid- and downstream operation of the industry had been completely developed. Taiwan, together with Hong Kong, Italy and South Korea were regarded as the world’s top four exporters of textile products at that time.

During and after the 1980s, the sector saw a decline which was caused by numerous unfavourable conditions such as export quota, a surge in the price of raw materials, rising wages, the emergence of environmental awareness, appreciation of Taiwan dollar (NTD) and the newly rising manufacturing countries joining the world market competition with their low-cost production. The sector in Taiwan consequently moved factories to countries of Southeast Asia and South America, and Mainland China. The growth rate of the sector’s production values experienced a plunge in the 10 years during the 1990s.

Upon its entry to the WTO in 2002, Taiwan has encountered competition on a global scale. With the worldwide financial tsunami occurring in 2008, the industry suffered further aggravation. However, Taiwan remained the world’s 6th exporter of textile products and the 29th exporter of garments in 2009, with its functional and environmental protection related textile products particularly still ranked high in the world. Yet the sector’s production and sales values have seen a continuous drop in recent years, and thus its outlook is now wait-and-see.

The heavy blow by the Covid-19 pandemic in 2020 has caused an obvious downturn of the import and export values of Taiwan’s textile products. But the sector experienced a gradual rebound in the second half of the year when the pandemic was alleviated. In response to the challenges brought by the pandemic, some large enterprises have shifted production to anti-pandemic items while some have input fashionable elements into the fabric they are producing. Some have developed new anti-pandemic materials, which has bred good profits and even becomes a new trend for future development of these enterprises.